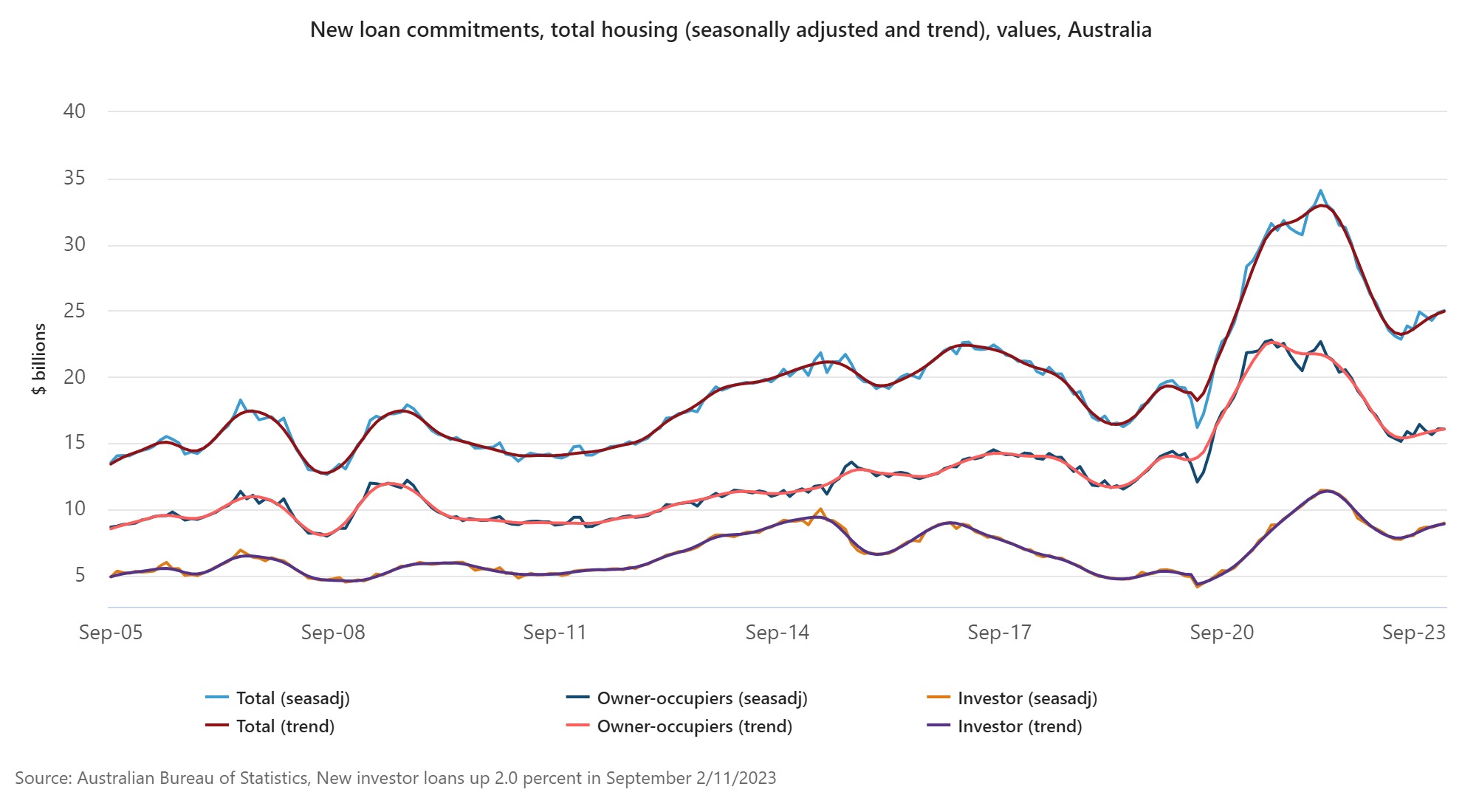

Investor activity have carried the lending market for September, with new investor loan commitments rising 2.0%, which is 2.6% higher than last year, according to the latest ABS lending indicators.

However, there was only a small uptick in new loan commitments overall at the same time borrowers switching lenders in search of a better deal dries up in spring.

A total of $25.01 billion in new home and investment property loans were taken out in September, which is up by a very modest 0.6% from August.

New loan commitments for owner occupier borrowers actually fell 0.1% over the month to $16.06 billion, while investment lending increased to reach $8.95 billion.

Mish Tan (pictured above), ABS head of finance statistics, said since February 2023, the value of new housing loan commitments have trended upwards, with total growth in investor loans exceeding owner-occupier loans.

“That said, the total value of new housing loan commitments in recent months remains below the all‑time highs seen throughout the COVID-19 pandemic,” Tan said.

“The value of new investor loan commitments increased across most states and territories this month, driven by rises in Victoria ($127m) and New South Wales ($77m).”

The subdued start to the selling season follows months of below-average property listings, according to CoreLogic. However, it also reports that the flow of new capital city properties listed for sale has started to ramp up since June.

Canstar’s finance expert Steve Mickenbecker (pictured above right) said more property listings seeping into the market were likely to boost loan commitments in the coming months.

“Undeterred by higher interest rates and in spite of the value of new lending falling 4.7% below September 2022, Australian house prices are reported by CoreLogic to be only just short of their all-time high on the back of eight months of frenetic increases,” said Mickenbecker, Canstar's group executive, financial services.

Mickenbecker said September's new lending commitments rose by just 0.6% for the month, but with more stock coming onto the market in a strengthening but not yet booming spring property season, a stronger recovery “could be ahead of us”.

“It’s also likely to slow the pace of house price rises, which have been fed by undersupply,” he said.

“Lending to owner occupiers is actually down 8.4% over the year, as repayment affordability probably holds buyers back. Investors are not as challenged and for investment lending to be growing at 2% for the month they must be confident that the price recovery is sustainable.”

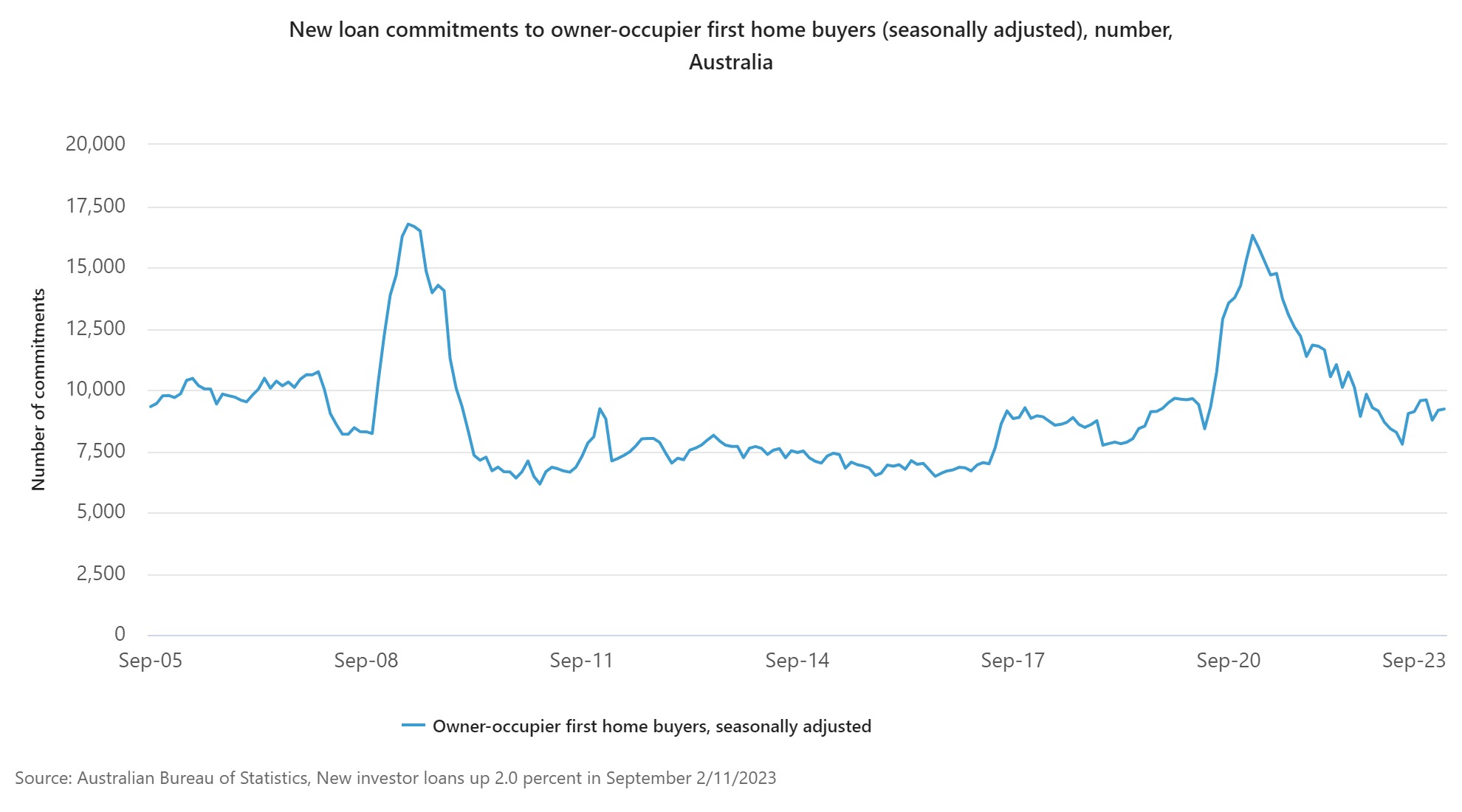

After months of no data as the ABS worked on its statistical modelling, first home buyers continued to return to the market, with the number of loans up 0.5% for the month after August's 4.6% leap.

The number of loans is now 9,213, up 18% from February's six-year low and makes up around 36% of the number of owner occupied dwellings, seasonally adjusted.

“It looks like they will again be facing headlong competition from investors as they did after their peak since the global financial crisis at 16,298 in January 2021,” said Mickenbecker.

The number of mortgage holders making the move to a new lender fell by 7.8%, with $18.5 billion in loans switched to a new lender in September when compared to the month prior. However, this is still 1.5% higher compared to a year ago.

The 4-percentage point increase in the cash rate since April 2022 has seen the average variable rate for existing borrowers rise from 2.98% to reach an estimated 6.98% following the most recent cash rate rise in June 2023.

Canstar analysis showed this adds approximately $1,217 to repayments on a $500,000 loan over 30 years or $2,435 on a $1 million loan.

Repayments could rise again next week if the Reserve Bank lifts the cash rate to 4.35% off the back of higher-than-expected inflation figures for the September quarter.

Another 0.25 percentage point cash rate rise will add $84 to repayments on a $500,000 loan over 30 years and increase repayments since April 2022 by 62% or $1,301 per month taking the monthly repayment up to $3,404.

Commenting on the fall in borrowers switching lenders for a better deal, Mickenbecker said the slowdown in borrowers switching lenders came as a surprise with the interest rate inundation they have had.

“Hopefully, borrowers have put the pressure on their existing lender for a significant rate cut to ease the burden,” he said. “Owner occupiers have been most reticent to switch lenders, with external refinancing hitting its largest monthly percentage decrease since January 2022.

“This is potentially down to a lack of confidence amongst borrowers that they will qualify for a loan with a new lender.”

“While the rate bargains of 18 months ago are long gone, borrowers paying an average variable rate of 6.98% can give themselves a 1.49% rate cut by moving to one of the lowest rates on Canstar. No one should be ignoring this interest rate relief after the shock of the last 18 months.”

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.