The NAB Residential Property Index has sustained its upward trajectory in the third quarter, as home prices continued to rebound across most of the country, and national rents remained on the rise amidst historically low vacancy rates.

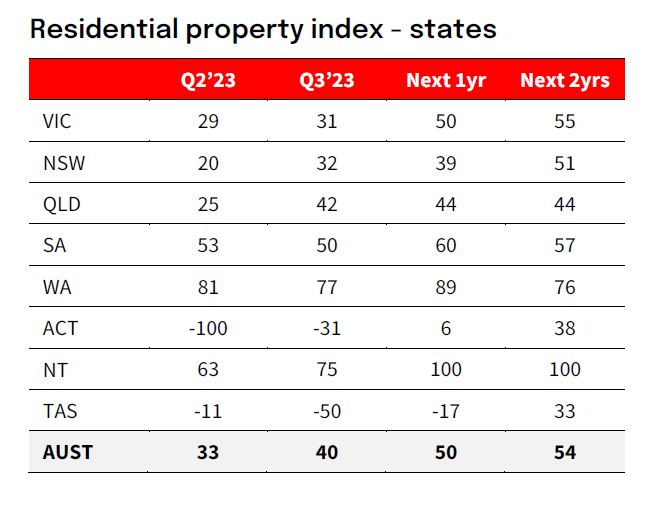

The index rose for the third consecutive quarter to +40 points, well above both the previous quarter’s +33 points and the +9 points recorded in the same period last year and exceeding the survey average of +18 points.

Housing market sentiment varied widely across regions, with Tasmania at -50 points, the ACT at -31 points, while it rose in Victoria (+31), NSW (+32), Queensland (+42), and the Northern Territory (+75), and softened in Western Australia (+77) and South Australia (+50), though both states still outperformed the national average.

Alan Oster (pictured above), NAB's group chief economist, added that confidence among surveyed property professionals has reached its highest level in around two years, reflecting stronger expectations for a housing market recovery over the next few years.

NAB’s one-year confidence measure lifted to +50 pts in Q3, with the two-year measure at +54 pts. Property professionals operating in WA and the NT are the most confident, and in the ACT and TAS the least confident.

Forecasts for national house prices have also been raised, with property professionals now tipping a 1.5% rise in the next 12 months and a 2.4% lift in two years, with the strongest expectations in Western Australia and the Northern Territory.

In terms of rental growth, expectations for the next 12 months and in two years’ time eased slightly to a still healthy 3% in Q3, from 4% for both periods in the previous survey, with rents still on the rise across most parts of the country.

Property professionals continued to report highly constrained supply conditions in housing rental markets, with a net 79% assessing the balance between supply and demand as undersupplied, compared to 83% in the previous quarter. They also indicated undersupply in all states, ranging from 97% in Western Australia to 63% in NSW during Q3.

The Q3 market share for first-home buyers in new housing markets plunged to a near eight-year low of 30.3%, with declines in both FHB owner-occupiers (20.9%) and investors (9.4%). Conversely, the market share of sales to resident owner-occupiers (excluding FHBs) continued to rise to a near 11-year high of 41.8%. Domestic investors also had a bigger role, reaching a 16.5% market share, though still below levels seen prior to the current interest rate cycle.

For most property professionals, construction costs remained a major barrier to starting new residential development projects, with roughly 78% expressing concern, followed by rising interest rates (55%) and delays in obtaining planning permits (46%).

In Q3, buying activity in established housing markets continued to be led by owner-occupiers (excluding FHBs), with their market share unchanged at below average 45.8%. FHBs also saw a decline in their overall market share to 31%, as FHB owner-occupiers fell to 23.5%, and FHB investors hit a survey low of 7.5%. The market share of local investors, however, edged up to 17.9%, which was still well below average.

“Rising interest rates continues to be identified as the biggest constraint for buyers of existing property nationally in Q3 – though weighing a little less heavily on buyers than in Q2,” Oster said. “Lack of stock is now seen as the next biggest hurdle for buyers overall, particularly in WA.

“Access to credit and price levels were next and assessed as a ‘significant’ impediment for buyers in all states (bar WA). Employment security and returns from other investments continue to have the least influence on home buyers, with their impact considered only ‘somewhat significant’ in all states.”

NAB’s latest survey also indicated a growing presence of foreign buyers in the Australian housing market in recent quarters.

Total market sales to foreign buyers in new housing markets were estimated to reach a five-and-a-half year high of 10.1% in Q3, raising the survey average for the first time since mid-2018. This was driven by heightened activity in NSW, where market sales rose to 14.9% from 9.2% in Q2, and Victoria, up to 11.3% from 7.4% the previous quarter. In the established housing markets, the share of foreign buyers reached a four-year high of 4.1% in Q3, with all states seeing increases, led by Victoria at 5%

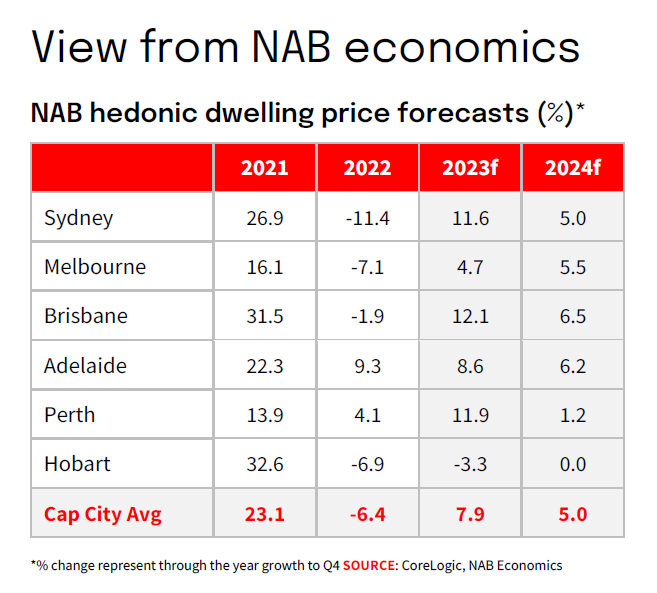

NAB upgraded its dwelling price projections for 2023 and 2024, on the back of stronger-than-expected performance in the last three months. Capital city dwelling prices are now anticipated to rise by around 8% by year-end and a further 5% the following year, as the strong housing demand relative to supply continues to offset the effects of rising interest rates.

On interest rates, NAB continued to expect the Reserve Bank to lift rates to 4.35% in November, with the likely upside in the Q3 CPI a significant factor, then keep them on hold for an extended period before easing them back to neutral in the second half of next year.

“More broadly, we expect the impact of higher rates and inflation to continue to see sluggish growth in consumer demand and below trend growth to see some easing labour market pressures and for inflation to continue to moderate back towards the RBA’s target band over the next year or so,” Oster said.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.